Investor Conference Call on March 21, 2024 at 8:00 a.m. ET

TORONTO, CANADA – March 20, 2024 – Baylin Technologies Inc. (TSX: BYL) (the “Company” or “Baylin”), a diversified global wireless technology company focused on the research, design, development, manufacture, and sale of passive and active radio frequency products, satellite communications products, and supporting services, today announced its financial results for the three and twelve months ended December 31, 2023. All amounts are stated in Canadian dollars unless otherwise indicated.

The Company has hired an investment banker to facilitate the divestiture of our Mobile and Network (“M&N”) business line in this calendar year. As a result, for the purpose of reporting our results, continuing operations now comprise three business lines: (a) Embedded Antenna; (b) Wireless Infrastructure; and, (c) Satcom, while the M&N business line is being reported as “held for sale”.

FISCAL YEAR SUMMARY

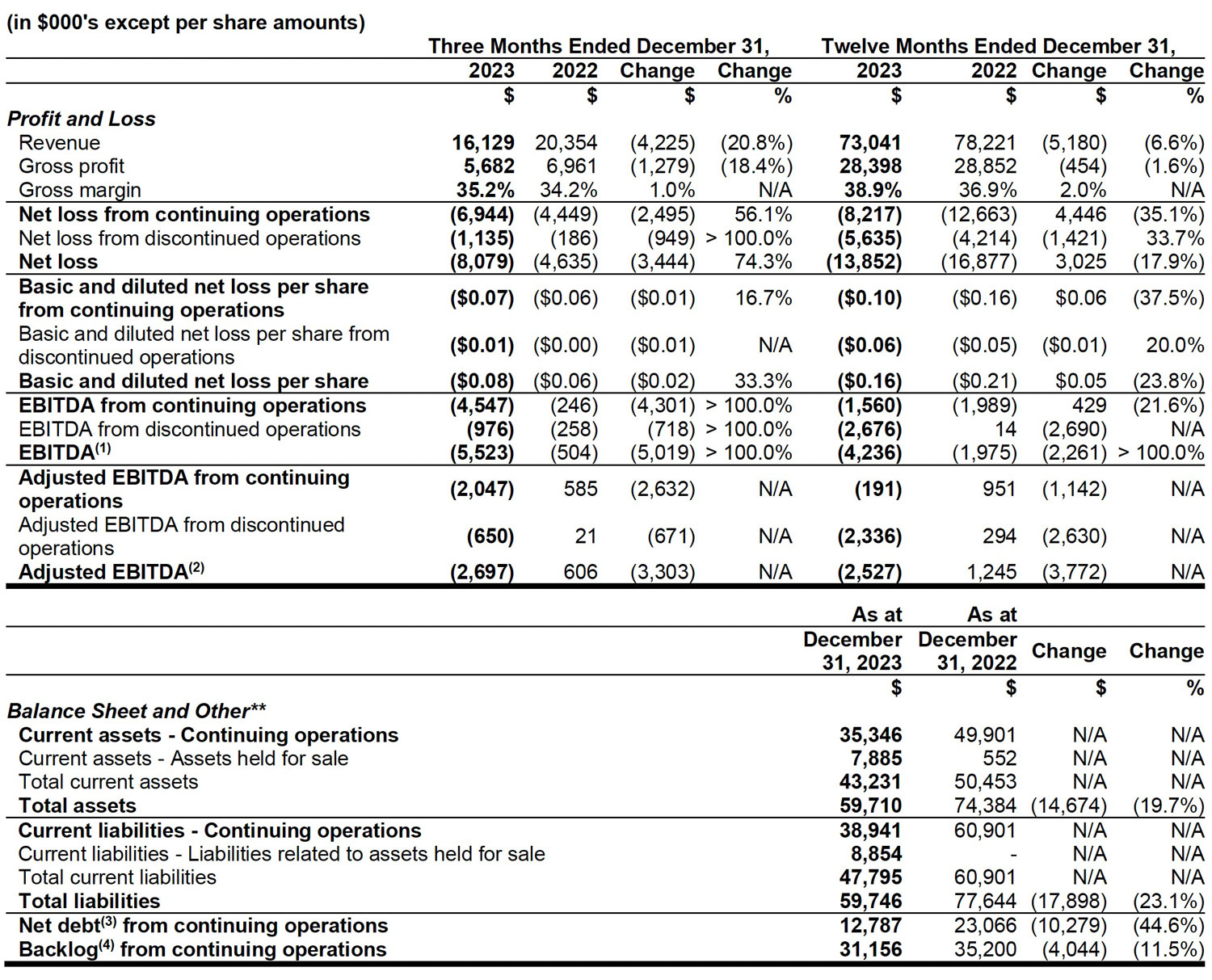

- Revenue from continuing operations of $73.0 million in fiscal 2023, a decrease of $5.2 million or 6.6% compared to fiscal 2022. The decrease was primarily due to a decrease in sales volumes in the Embedded Antenna and Wireless Infrastructure business lines compared to the prior fiscal year, partially offset by an increase in sales volumes in the Satcom business line.

- Gross margin from continuing operations of 38.9% in fiscal 2023 compared to 36.9% in fiscal 2022, despite gross profit from continuing operations of $28.4 million being $0.5 million less than fiscal 2022. The improved gross margin resulted from a balanced product mix including sales of newly launched products, changes in pricing strategy, and a data driven focus on contribution margin at the business line level. In fiscal 2023, the improvement was mainly generated by: (i) stronger revenue recovery in the Satcom business line; (ii) favourable product mix, including the new multibeam and innovative antenna portfolio in the Wireless Infrastructure business line; and, (iii) consistent operational efficiency in the Embedded Antenna business line.

- Adjusted EBITDA(2) from continuing operations of -$0.2 million in fiscal 2023, a decrease of $1.2 million compared to $1.0 million in fiscal 2022. The decrease in Adjusted EBITDA from continuing operations in fiscal 2023 was primarily due to the decrease in revenue and gross profit as discussed above, partially offset by a decrease in operating expenses compared to the prior fiscal year.

- Adjusted EBITDA from discontinued operations of -$2.3 million in fiscal 2023, a decrease of $2.6 million compared to $0.3 million in fiscal 2022. The decrease in Adjusted EBITDA from discontinued operations was mainly due to the decrease in revenue and gross profit of the M&N business line as a result of across-the-board production volume reductions at its principal customer in fiscal 2023.

- Net loss from continuing operations of $8.2 million in fiscal 2023 compared to a net loss of $12.7 million from continuing operations in fiscal 2022. The net loss from continuing operations in fiscal 2023 was primarily due to an operating loss of $5.4 million, interest expenses and income tax expenses. On a per share basis, a net loss of $0.10 per share in fiscal 2023 compared to a net loss of $0.16 per share in fiscal 2022.

- Net loss from discontinued operations of $5.6 million in fiscal 2023 compared to a net loss of $4.2 million from discontinued operations in fiscal 2022. The net loss from discontinued operations in fiscal 2023 was mainly due to an operating loss of $5.0 million as well as other finance expenses in the M&N business line. On a per share basis, a net loss of $0.06 per share in fiscal 2023 compared to a net loss of $0.05 per share in fiscal 2022.

- Net debt(3) from continuing operations of $12.8 million as at December 31, 2023, a decrease of $10.3 million from December 31, 2022, mainly attributable to a decrease in non-cash working capital in fiscal 2023 as well as full repayment of the Company’s term loan from proceeds of a rights offering and a private placement of preferred shares in December 2023.

- Backlog(4) from continuing operations of $31.2 million at December 31, 2023 compared to $35.2 million at December 31, 2022. The decrease was due to a lower level of backlog across all business lines as a result of a challenging macroeconomic environment during fiscal 2023. Backlog increased to $34.7 million at March 13, 2024 as a result of increased order intake levels across all business lines in the first quarter of 2024.

FOURTH QUARTER SUMMARY

- Revenue from continuing operations of $16.1 million in the fourth quarter of 2023, a decrease of $4.3 million or 20.8% compared to the fourth quarter of 2022. The decrease in revenue in the fourth quarter of 2023 was mainly due to the reasons noted above.

- Gross margin from continuing operations of 35.2% in the fourth quarter of 2023 compared to 34.2% in the fourth quarter of 2022 despite gross profit from continuing operations of $5.7 million being $1.3 million less than the fourth quarter of 2022. The improved gross margin in the fourth quarter of 2023 was primarily attributable to stronger revenue recovery and favourable product mix in the Satcom business line.

- Adjusted EBITDA from continuing operations of -$2.0 million in the fourth quarter of 2023, a decrease of $2.6 million compared to the fourth quarter of 2022. The decrease in Adjusted EBITDA from continuing operations in the fourth quarter of 2023 was mainly due to the decrease in revenue and gross profit as discussed above.

- Adjusted EBITDA from discontinued operations of -$0.7 million in the fourth quarter of 2023, a decrease of $0.7 million compared to the fourth quarter of 2022. The decrease in Adjusted EBITDA in the fourth quarter of 2023 from discontinued operations was mainly due to the reasons noted above.

- Net loss from continuing operations of $6.9 million in the fourth quarter of 2023 compared to a net loss of $4.4 million from continuing operations in the fourth quarter of 2022. The net loss from continuing operations in the fourth quarter of 2023 was primarily due to an operating loss of $5.3 million as well as interest expenses. On a per share basis, a net loss of $0.07 per share in the fourth quarter of 2023 compared to a net loss of $0.06 per share in the fourth quarter of 2022.

- Net loss from discontinued operations of $1.1 million in the fourth quarter of 2023 compared to a net loss of $0.2 million from discontinued operations in the fourth quarter of 2022. On a per share basis, a net loss of $0.01 per share in the fourth quarter of 2023 compared to a net loss of close to $0.00 per share in the fourth quarter of 2022.

SELECTED FINANCIAL INFORMATION

The table below discloses selected financial information for the periods indicated.

- See “Non-IFRS Measures”. EBITDA refers to operating income (loss) plus depreciation and amortization.

- See “Non-IFRS Measures”. Adjusted EBITDA refers to EBITDA plus the sum of: a) acquisition expenses; b) fair value step-up of inventory acquired as part of an acquisition; c) expenses for litigation relating to acquisition agreements; d) expenses relating to planned restructuring following an acquisition; e) impairment of fixed and intangible assets (including goodwill) following an acquisition; f) expenses to permanently close or relocate a facility, shut down a line of business, eliminate positions; g) expenses related to corporate re-organization; and, h) non-cash compensation.

- See “Non-IFRS Measures”. Net debt refers to total bank indebtedness less cash and cash equivalents.

- See “Non-IFRS Measures”. Backlog refers to the value of unfulfilled purchase orders placed by customers.

** Balance Sheet as at December 31, 2023 reflects the reclassification of all assets and liabilities of the M&N business line into “Assets held for sale” and “Liabilities related to assets held for sale”, respectively. Such assets and liabilities are classified as current. Balance Sheet as at December 31, 2022 does not reflect such reclassification, which makes the comparison against the current fiscal year-end results not applicable (except for “Total assets” and “Total liabilities”).

A copy of the Company’s consolidated financial statements for the three and twelve months ended December 31, 2023 and corresponding management’s discussion and analysis (the “MD&A”) are available under the Company’s profile on SEDAR+ at www.sedarplus.ca.

RECENT DEVELOPMENTS

Products

Galtronics multibeam antennas continue to demonstrate their class-leading performance, building on earlier successes in 2023 and now into 2024. Notably, they were chosen for Allegiant Stadium in Los Vegas, Nevada, host venue for the 2024 Super Bowl. The antennas are uniquely able to handle large scale events and venues in a cost-effective manner for wireless carriers. Additionally, they offer comparable performance to lens-type technology at a more economical price point and provide beam stability across frequency bands to ensure a better user experience. Galtronics is the only company approved by the three major US telecom carriers for these innovative products, opening up additional revenue opportunities for the remainder of 2024.

Satcom continues to expand and develop its solid state power amplifier systems. Summit III, its latest system, is based on the compact and soft-fail redundant Genesis amplifier, which is available in Ku-band architecture of 200 watts to 500 watts and also a C-band architecture in 500 watts. In February 2024, Satcom received an order for the first phase of a Direct-to-Home satellite broadcast network from a major cable operator in India. The first phase of the order consists of four 3.2kW Summit III systems, each comprised of eight 500 watt C-band amplifiers with an order value of approximately $2.7 million. The second phase of the order is expected in late Spring 2024 and the third phase of the order is expected in March 2025.

Credit Facilities

The Company agreed with its principal lenders, Royal Bank of Canada and HSBC Bank Canada, to further amendments to the Credit Agreement governing the Credit Facilities, including an extension to the maturity date of the Revolving Facility from March 31, 2024 to June 30, 2024.

Financings

In December 2023, the Company completed two financings — a rights offering and a private placement.

On November 10, 2023, the Company announced an offering (the “Rights Offering”) of rights (the “Rights”) to shareholders of record of its common shares on November 21, 2023 under which holders were entitled to receive one Right for each common share held, resulting in the issuance of 88,547,818 Rights. Each Right entitled the holder to purchase one common share at a subscription price of $0.19, a 17.4% discount to the closing price of the common shares on the TSX on the day before the announcement. The Rights Offering expired on December 19, 2023. The purpose of the Rights Offering was to raise proceeds to repay term indebtedness under the Company’s credit facilities.

The Company received subscriptions for 62,186,516 common shares, including subscriptions for 54,626,763 common shares from 2385796 Ontario Inc., the Company’s largest shareholder (the “Principal Shareholder”), and a related party of the Principal Shareholder, resulting in proceeds to the Company of approximately $11.8 million.

On December 29, 2023, the Company completed a private placement (the “Private Placement”) of a new series of its preferred shares to the Principal Shareholder. The Principal Shareholder subscribed for 68,000 10% Cumulative Redeemable Retractable Series A Preferred Shares (the “Series Preferred Shares”) at a price of $25.00 per share, resulting in proceeds to the Company of $1.7 million.

The Company used the proceeds from the Rights Offering and the Private Placement to repay in full term indebtedness owed to its principal Canadian lenders, which was due on December 29, 2023.

OUTLOOK

The Company continued to navigate a challenging macroeconomic environment during the fourth quarter of 2023, resulting in lower revenue, gross margin and Adjusted EBITDA than each of the previous three quarters. While our overall performance continued to be significantly negatively affected by the results of our M&N business line, we also experienced softness in our Embedded Antenna and Wireless Infrastructure business lines. Satcom’s performance remained in line with expectations.

We continue to prioritize product mix, emphasizing products that generate higher margins and gross profit, with a view to maintaining and growing Adjusted EBITDA. The macroeconomic environment and the effect of high interest rates are expected to remain an issue for our business in the short term. These factors could affect our volume of orders and revenue as well as causing pushouts of orders from customers. However, we expect to see signs of improvement across all business lines in 2024, particularly in the Embedded Antenna business line, starting in the first quarter of 2024.

The Company is continuing its efforts to recapitalize its balance sheet by reducing indebtedness and refinancing its revolving credit facility. The repayment of our term indebtedness at 2023 year-end was a major milestone in those efforts. Moving forward, the Company is looking to replace its current revolving facility with an asset-based loan, which will reduce annual debt service costs by eliminating annual principal payments, freeing up cash for investment in the business.

Embedded Antenna Business Line

The Embedded Antenna business line was adversely affected by macroeconomic conditions in 2023, especially in the fourth quarter, resulting in materially lower sales volumes, a result that was reflected industrywide. We were also affected by lower margins caused by changes in product mix. These conditions are not likely to recur in 2024 and we expect to see a slow recovery in demand for embedded products, including as service providers shift from Wi-Fi 6 to Wi-Fi 7. We are already seeing evidence of increased demand. For now, we expect the Embedded Antenna business line will continue to perform reasonably well in 2024, in line with 2023. Its performance depends on the ability of the home networking, public safety and automotive markets to remain resilient in the face of the economic pressures. The number of active bids for 2024 projects remains at a very strong level for the business.

Wireless Infrastructure Business Line

We expect the Wireless Infrastructure business line will perform well in 2024, up from 2023, with improvements in revenue, gross margin and Adjusted EBITDA. We are looking to build on the sales success of its higher margin multibeam and innovative small cell antennas as well as the strong pace of stadium deployments. We expect that our new higher margin multibeam and innovative small cell antennas will open up new global opportunities to drive sales with wireless carriers and third-party operators who operate wireless mobile networks for their customers. We are continuing to expand into new markets, particularly in areas in Europe where we have not previously had sales. Although we experienced some pull-back on spending by wireless carriers and infrastructure customers broadly in the fourth quarter of 2023, we expect to continue to grow and take market share by focusing on our unique competitive advantages. We do expect to see increased spending by carriers on small cells in 2024, which will drive further volumes for the business.

Satcom Business Line

The Satcom business line continues to demonstrate consistent demand with capital spending by our customers.

Satcom benefited from the capital build cycles of satellite operators and others in the Satcom ecosystem in 2023. We saw that major programmatic opportunities continued to be resilient, particularly for high powered amplifiers, and we expect this will continue in 2024. We do see softness in the commercial lower power market, but given our focus on higher power opportunities, the business will continue to have resiliency in the coming year. We further expect that our new Genesis and Summit lines of solid-state power amplifiers will generate sales from clients due to the improvements in performance, monitoring, and failover they provide over our older technology and our competition. Importantly, these new amplifiers are consistent in architecture, meaning they will allow the business to simplify supply chain over time and thereby improve efficiencies in manufacturing.

We continue to see opportunities for growth in sales for military and other government-related uses as many western countries continue to maintain high levels of defence and scientific spending. Given the technology upgrades within our product portfolio, we expect to continue our strong sales volumes while we work to improve our overall margin attainment.

Overall, we expect revenue and Adjusted EBITDA in 2024 will be incrementally stronger than 2023. The Satcom business line continues to demonstrate a strong order book with improving margins. Improving production efficiencies in our facilities in order to address the backlog and improve overall revenue attainment remains an important priority, particularly in our Kirkland, Quebec, facility. In order to alleviate some of the production backlog in that facility, we have begun production of high-power amplifiers in our State College, Pennsylvania, facility.

Mobile and Network (formerly, Asia Pacific) Business Line

The M&N business line continues to face significant challenges due to continuing large production volume reductions at its principal customer. Those reductions reflect a contraction in the customer’s smartphone market, due in part to consumers upgrading their smartphones with less frequency, as well as competitive pressures faced by the customer. Global shipments of smartphones experienced a year-over-year decline in 2023 although demand increased in the fourth quarter. The customer is also facing weaker demand for its other products such as tablets, smart watches, and other wirelessly connected devices.

Management has been taking steps to limit the adverse effect this has had on the M&N business. We continue to focus on reducing or eliminating operating and other costs while work is done to diversify the revenue base. M&N has been awarded other revenue-generating projects, but several have been hampered by the adverse economic environment in the Korean market, and any resulting benefit is not likely to be seen until the second half of 2024.

Given these ongoing challenges, the Company has hired an investment banker to facilitate the divestiture of the M&N business line in this calendar year.

INVESTOR CONFERENCE CALL

Baylin will hold a conference call on March 21, 2024 at 8:00 a.m. (ET) to discuss its financial results for the three and twelve months ended December 31, 2023. The conference call will be hosted by Leighton Carroll, Chief Executive Officer, and Dan Nohdomi, Chief Financial Officer. All interested parties are invited to participate using the dial-in details provided below.

Date: March 21, 2024

Time: 8:00 a.m. (ET)

Dial-in Number: 888-664-6392 or 416-764-8659

Conference ID#: 73479294

Rapid Connect: To instantly join the conference call by phone, please use the following URL to easily register and be connected into the conference call automatically: https://emportal.ink/3IeIKTa

Webcast: This call is also on webcast and can be accessed at: https://app.webinar.net/l9LV86dNDR4

FORWARD-LOOKING INFORMATION AND STATEMENTS

This press release includes forward-looking information and forward-looking statements (together, “forward-looking statements”) within the meaning of applicable securities laws. Forward-looking statements are not statements of historical fact. Rather, forward-looking statements are disclosure regarding conditions, developments, events or financial performance that we expect or anticipate may or will occur in the future including, among other things, information or statements concerning our objectives and strategies to achieve those objectives, statements with respect to management’s beliefs, estimates, intentions and plans, and statements concerning anticipated future circumstances, events, expectations, operations, performance or results. Forward-looking statements can be identified generally by the use of forward-looking terminology, such as “anticipate”, “believe”, “could”, “should”, “would”, “estimate”, “expect”, “forecast”, “indicate”, “intend”, “likely”, “may”, “outlook”, “plan”, “potential”, “project”, “seek”, “target”, “trend” or “will” or the negative or other variations of these words or other comparable words or phrases and is intended to identify forward-looking statements, although not all forward-looking statements contain these words.

The forward-looking statements in this press release include statements concerning the effect of the macro-economic environment on our business, increased material costs due to inflationary pressures, higher interest rates, the outlook for our business lines, particularly M&N, and other disruptions on their financial performance. Forward-looking information and statements are based on certain assumptions and estimates made by us in light of the experience and perception of historical trends, current conditions, expected future developments, including projected growth in the sales of passive and active radio frequency and satellite communications products, and supporting services, and other factors we believe are appropriate and reasonable in the circumstances, but there can be no assurance that such assumptions and estimates will prove to be correct.

Many factors could cause our actual results, level of activity, performance or achievements or future events or developments to differ materially from those expressed or implied by the forward-looking statements, including the risk factors discussed in the Company’s most recent Annual Information Form, which is available under the Company’s profile on SEDAR+ at www.sedarplus.ca. All the forward-looking statements made in this press release are qualified by these cautionary statements and other cautionary statements or factors in this press release. There can be no assurance that the actual results or developments will be realized or, even if substantially realized, will have the expected consequences to, or effects on, the Company. Unless required by applicable securities law, the Company does not intend and does not assume any obligation to update any forward-looking statements.

NON-IFRS MEASURES

This press release includes a number of measures that are not prescribed by International Financial Reporting Standards (“IFRS”) and as such may not be comparable to similar measures presented by other companies. We believe these measures are commonly employed to measure performance in our industry and are used by analysts, investors, lenders and interested parties to evaluate financial performance and our ability to incur and service debt to support business activities. While management of the Company believes that non-IFRS measures provide helpful supplemental information, they should not be considered in isolation as an alternative to net income, cash flows generated by operating, investing or financing activities, or other financial statement data presented in accordance with IFRS. For further information, see “Non-IFRS Measures” on page 3 of the MD&A.

ABOUT BAYLIN

Baylin Technologies Inc. is a diversified global wireless technology company focused on the research, design, development, manufacture, and sale of passive and active radio frequency products, satellite communications products, and supporting services.

For further information, please visit www.baylintech.com.